Table Of Content

They are basic debt-to-income ratios (DTI), albeit slightly different and explained below. For more information about or to do calculations involving debt-to-income ratios, please visit the Debt-to-Income (DTI) Ratio Calculator. This is a separate calculator used to estimate house affordability based on monthly allocations of a fixed amount for housing costs. Fixed-rate loans have the same interest rate for the entire duration of the loan. That means your monthly home payment will be the same, even for long-term loans, such as 30-year fixed-rate mortgages. Two benefits to this mortgage loan type are stability and being able to calculate your total interest on your home upfront.

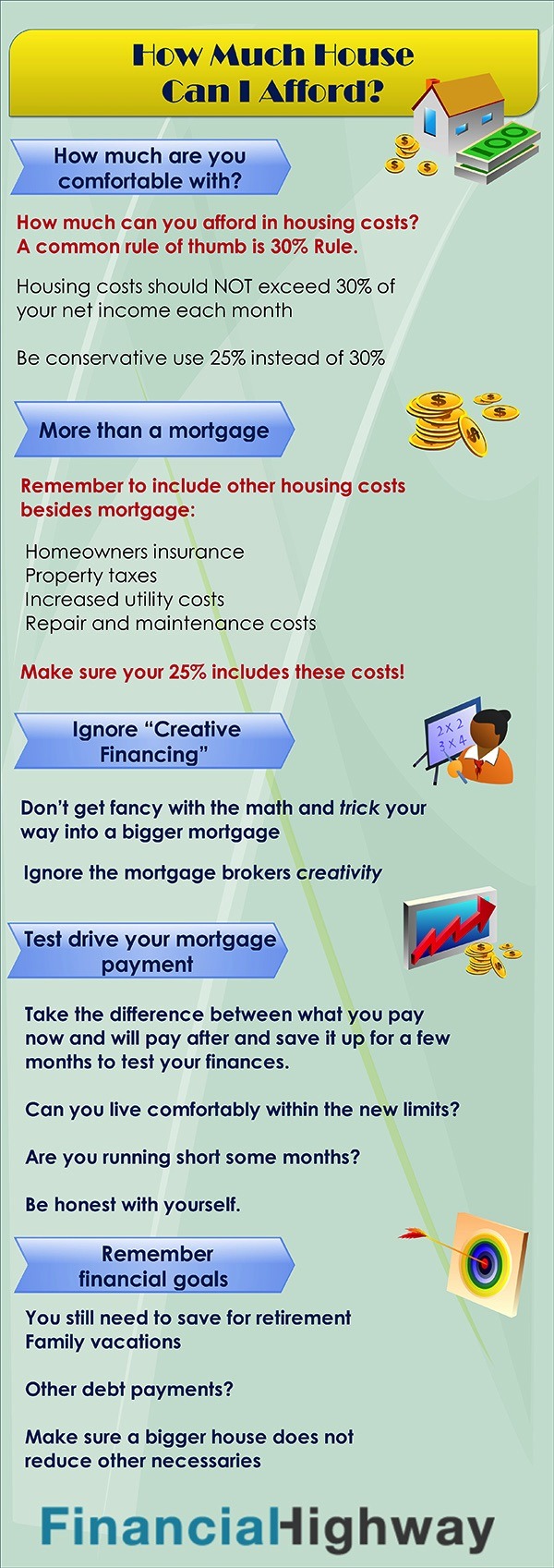

Conventional Loans and the 28/36 Rule

Adjustable-rate mortgages (ARMs) have interest rates that can change over time. Typically, they start out at a lower interest rate than a fixed-rate loan and hold that rate for a set number of years before changing interest rates from year to year. For example, if you have a 5/1 ARM, you will have the same interest rate for the first 5 years, and then your mortgage interest rate will change from year to year. The main benefit of an adjustable-rate loan is starting off with a lower interest rate to improve affordability. Gross monthly income is the total amount of money you earn in a month before taxes or deductions.

Today's mortgage and refinance rates

There is something to be said for the idea of not maxing out your credit possibilities. If you look at houses that are priced somewhere below your maximum, you leave yourself some options. For one, you will have room to bid if you end up competing with another buyer for the house. As an alternative, you’ll have money for renovations and upgrades. A little work can transform a home into your dream house — without breaking the bank.

Mortgage rates top 7% — is this a good time to buy a house? - Yahoo Finance

Mortgage rates top 7% — is this a good time to buy a house?.

Posted: Thu, 18 Apr 2024 07:00:00 GMT [source]

Fixed rate vs adjustable rate

When lenders evaluate your ability to afford a home, they take into account only your present outstanding debts. They do not take into consideration if you want to set aside $250 every month for your retirement or if you’re expecting a baby and want to save additional funds. That’s a big deal, because mortgages backed by the Department of Veterans Affairs typically don’t require a down payment.

What Kind of House Can You Buy for $1500 a Month? - Real Estate

What Kind of House Can You Buy for $1500 a Month?.

Posted: Fri, 15 Dec 2023 08:00:00 GMT [source]

The higher your credit score, the better the interest rate you are offered; therefore, you might be able to own a higher priced home than someone with a low credit score. A general guideline when calculating how much home you can afford with your salary is to multiply your income by at least 2.5 or 3. This should give you an idea of the maximum housing price you can afford. While housing prices have jumped nationally, they can still vary widely in terms of affordability when broken down by local area.

The most important factors that determine how much you can afford:

Before you take on the maximum loan you can get and start looking at more expensive houses, consider these tips. If credit card debt is holding you back from getting to 36%, you might want to consider a balance transfer. You can transfer your credit card balance(s) to a credit card with a temporary 0% APR and pay down your debt before the offer expires. Read more on specialized loans, such as VA loan requirements and FHA loan qualification. In addition, take a look at the best places to get a mortgage in the U.S.

What are the most important factors to determine how much house I can afford?

Even though Martin can technically afford House #2 and Teresa can technically afford House #3, both of them may decide not to. If Martin waits another year to buy, he can use some of his high income to save for a larger down payment. Teresa may want to find a slightly cheaper home so she’s not right at that maximum of paying 36% of her pre-tax income toward debt. You’ll stop paying PMI when your mortgage reaches about 78% of the home’s value. Get Forbes Advisor’s ratings of the best mortgage lenders, advice on where to find the lowest mortgage or refinance rates, and other tips for buying and selling real estate.

Is your credit score in great shape, and is your overall debt load manageable? Do you have enough savings that a down payment won’t drain your bank account to zero? If your personal finances are in excellent condition, a lender will likely be able to give you the best deal possible on your interest rate. Reserves refer to the number of monthly mortgage payments you could make from your savings if you lost your job or experienced another event that impacted your ability to make your payment. Every loan program is different, but a good guideline is to keep at least 2 months’ worth of mortgage payments in your savings account.

Conventional loan (conforming loan)

Working towards achieving one or more of these will increase a household's success rate in qualifying for the purchase of a home in accordance with lenders' standards of qualifications. If these prove to be difficult, home-buyers can maybe consider less expensive homes. If not, there are various housing assistance programs at the local level, though these are geared more towards low-income households.

Note that you might not have to put down anything at all if you qualify for certain government loans. The Rocket Mortgage® Home Affordability Calculator gives you the option to see how much house you can afford, or how much cash you need for your down payment and closing costs. How large of a mortgage loan you can qualify for depends on how much debt a lender thinks you can take on as a borrower. This will ultimately determine how much house you’re able to afford.

The problem is that some people believe the answer to “How much house can I afford with my salary? ” is the same as the answer to “What size mortgage do I qualify for? ” What a bank (or other lender) is willing to lend you is definitely important to know as you begin house hunting.

Once moving to Alhambra head for a jog at Almansor Park and pick up some fresh produce at the Alhambra Farmers Market. In Los Angeles and Orange counties, the cap is $970,800, meaning you can buy a $1.2 million house with a 20% down payment. All three government-backed loans have mortgage limits, which is a handy way to help you stay in a healthy debt-budget range. Assessing how much you should spend on a house requires a bit of a look into your current and potentially future financial situation.

No comments:

Post a Comment